Bayesian changepoint wrapper (Barry-Hartigan product partition model)

Source:R/wrap-bayes.R

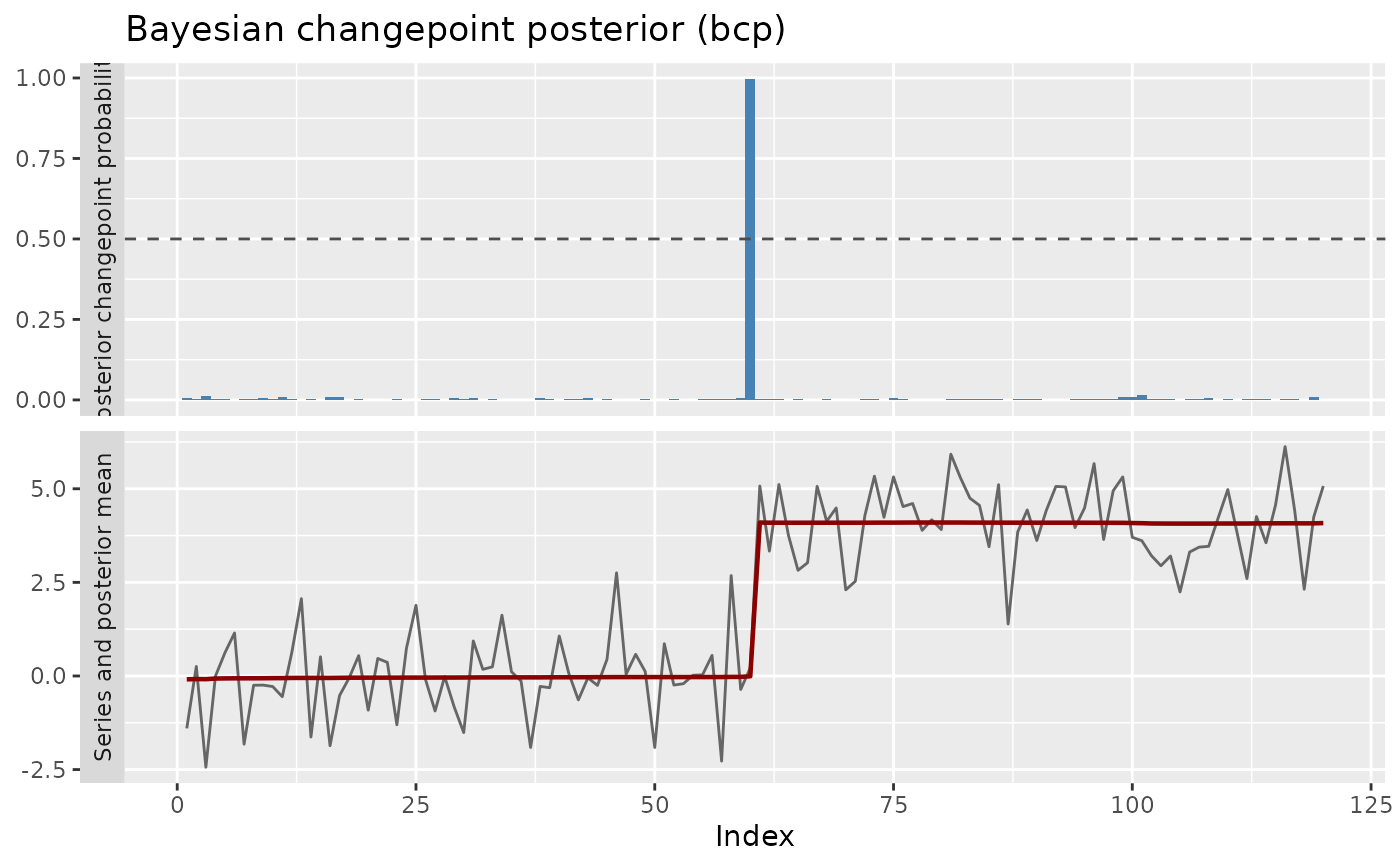

bcp_wrapper.RdWraps bcp::bcp(), the MCMC implementation (Erdman and Emerson, 2007)

of the Barry and Hartigan (1993) product partition model. The engine

returns a posterior probability of a changepoint at every location;

locations whose posterior probability reaches prob_threshold are

reported as changepoints, and the full probability profile is kept so that

ggcpt_posterior() can draw the classic two-panel posterior

plot.

Arguments

- x

A numeric vector.

- prob_threshold

Posterior probability cutoff in \((0, 1)\) above which a location is reported as a changepoint. Defaults to

0.5.- burnin

Number of burn-in MCMC iterations. Defaults to

50.- mcmc

Number of post-burn-in MCMC iterations. Defaults to

500.- seed

Optional seed for reproducibility of the MCMC run.

- ...

Additional arguments passed to

bcp::bcp().

Value

A ggcpt object. The changepoints tibble carries a

posterior_prob column, and the data tibble carries the

posterior mean in its fitted column.

References

Barry D, Hartigan JA (1993). “A Bayesian analysis for change point problems.” Journal of the American Statistical Association, 88(421), 309–319.

Erdman C, Emerson JW (2007). “bcp: An R package for performing a Bayesian analysis of change point problems.” Journal of Statistical Software, 23(3), 1–13.

Examples

res <- bcp_wrapper(c(rnorm(60), rnorm(60, 4)), seed = 2026)

#> Loading required package: bcp

#> Loading required package: grid

res$changepoints

#> # A tibble: 1 × 3

#> cp cp_value posterior_prob

#> <int> <dbl> <dbl>

#> 1 60 0.213 0.996

ggcpt_posterior(res)